Page 1 of 1

Capital gains tax and health insurance

Posted: Fri Mar 29, 2024 1:44 pm

by zeeshan

Hi,

It might be a stupid question however I still want to clarify it. I know that there's a flat 25% capital gains tax on stocks/ETs etc. and that German brokers already pay it if it exceeds the exemption order. My question is: Does it also affect statutory health insurance premium that I need to pay after the year end by my self? For clarification, I don't live on capital gains tax, I'm employed and I just invest the amount that's left after my expenses and I sell the stocks/ETFs to take advantage of the exemption limit and keep it to the limit but sometimes it exceed a little over it.

Is it something I need to consider or I'm just overthinking?

Re: Capital gains tax and health insurance

Posted: Fri Mar 29, 2024 2:55 pm

by PandaMunich

zeeshan wrote: ↑Fri Mar 29, 2024 1:44 pm

It might be a stupid question however I still want to clarify it. I know that there's a flat 25% capital gains tax on stocks/ETs etc. and that German brokers already pay it if it exceeds the exemption order.

My question is: Does it also affect statutory health insurance premium that I need to pay after the year end by my self?

For clarification, I don't live on capital gains tax, I'm employed and I just invest the amount that's left after my expenses and I sell the stocks/ETFs to take advantage of the exemption limit and keep it to the limit but sometimes it exceed a little over it.

Is it something I need to consider or I'm just overthinking?

You have to differentiate:

- Mandatory members of public health insurance (employees - but not employees who are beherrschende Gesellschaftsgeschäftsführer, self-employed who are in the Künstlersozialkasse and pensioners in receipt of a DRV pension who are in the KvdR = Krankenversicherung der Rentner = spent the 2nd half of their working life in German/EU/EEA/UK public health insurance):

You do not have to pay public health insurance&nursing insurance on what you took in from your capital assets.

- Voluntary members of public health insurance (everybody else):

Yes, you have to declare in the income questionnaire that your public health insurer sends you every year as additional monthly income and pay additional contributions on it:

1/12 * (what you took in per year from your capital assets - 51€)

So to be very clear: unlike the Finanzamt, which allows you to deduct the Sparerpauschbetrag of 1,000€ per year (up to 2022: 801€), your public health insurer only allows you to deduct 51€ per year in expenses (this TK article had a bit of a cookie problem in its GoogleTranslation, so just copy the German text into DeepL.com to get it translated into English): https://www.tk.de/techniker/leistungen- ... ng-2006786

Re: Capital gains tax and health insurance

Posted: Fri Mar 29, 2024 4:40 pm

by zeeshan

Thanks for explaining it. I still don't think I understood it all. According to the TK article you posed it says all type of income that you consume for a living counts towards contribution. It didn't differentiate between employees or voluntary members.

If I understood you correctly, then I don't have to pay contributions as I fall into the first category, correct?

Another thing, I just realized is would I fall into a voluntary member, if my salary exceed a threshold for a mandatory membership? I can't recall exactly but I think it was something like that I heard or read or had to accept in the past because I could have chosen the private insurance but I chose to stay with statutory. Does unemployment benefit from Agentur fuer Arbeit also affect it or make you a voluntary member? I think I usually read something about it when my insurance sent me a notice during a job switch.

And in case I do need to pay the contributions, I pay it at the year end, right? So for year 2024, I'll pay it in 2025 once I have a tax certificate from the broker.

I know a lot of questions. Sorry about that.

Re: Capital gains tax and health insurance

Posted: Fri Mar 29, 2024 7:05 pm

by PandaMunich

zeeshan wrote: ↑Fri Mar 29, 2024 4:40 pm

Thanks for explaining it. I still don't think I understood it all. According to the TK article you posed it says all type of income that you consume for a living counts towards contribution. It didn't differentiate between employees or voluntary members.

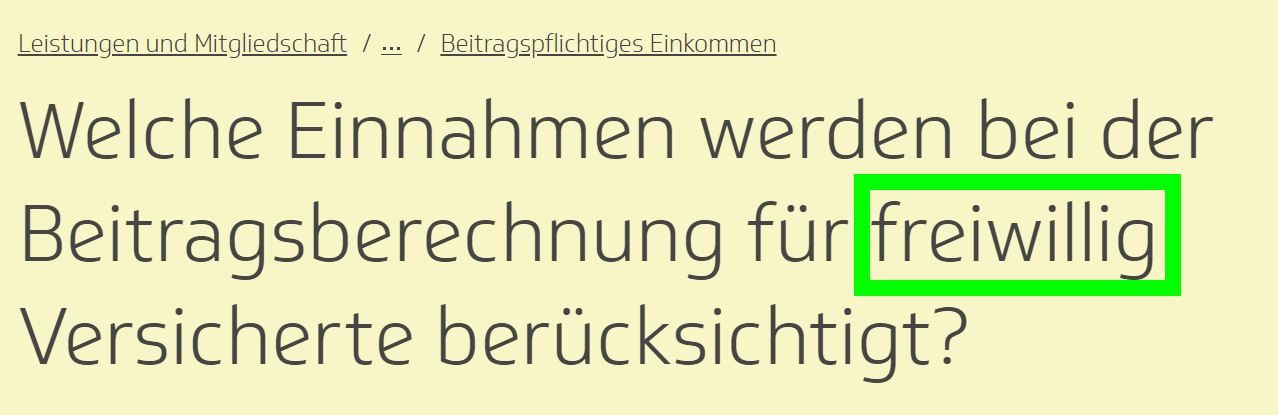

You missed the word "freiwillig" (= voluntary) in the TK headline:

- 2024-03-29 18_38_38-Welche Einnahmen werden bei der Beitragsberechnung für freiwillig Versicherte be.jpg (61.33 KiB) Viewed 7529 times

zeeshan wrote: ↑Fri Mar 29, 2024 4:40 pm

If I understood you correctly, then I don't have to pay contributions as I fall into the first category, correct?

Another thing, I just realized is would I fall into a voluntary member, if my salary exceed a threshold for a mandatory membership? I can't recall exactly but I think it was something like that I heard or read or had to accept in the past because I could have chosen the private insurance but I chose to stay with statutory.

If you are an employee who is a

high earner, i.e. your

yearly gross income is above the Versicherungspflichtgrenze (JAEG) of (in 2024)

69,300€:

https://de.wikipedia.org/wiki/Jahresarb ... e_Regelung

then you are no longer a mandatory member of German public health insurance, but a

voluntary member.

And as a voluntary member you have to contribute based on your

worldwide income, see the catalogue of all types of worldwide income that German public health insurance charges contributions on:

https://www.gkv-spitzenverband.de/media ... refrei.pdf

zeeshan wrote: ↑Fri Mar 29, 2024 4:40 pm

Does unemployment benefit from Agentur fuer Arbeit also affect it or make you a voluntary member? I think I usually read something about it when my insurance sent me a notice during a job switch.

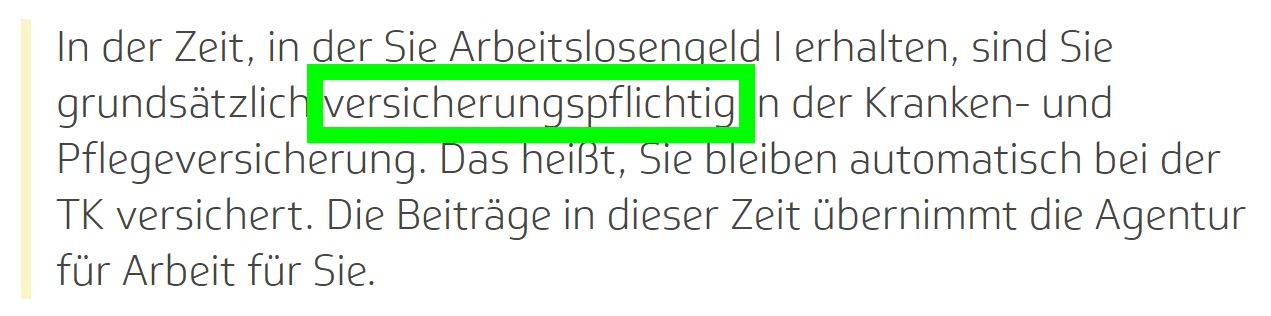

As soon as you become unemployed, you become a mandatory member of public health&nursing insurance, where before you had only been a voluntary member of public health insurance:

https://www.tk.de/techniker/leistungen- ... rt-2005726

It's that word "versicherungspflichtig" (= mandatory member of insurance) in the text that tells you:

- 2024-03-29 18_49_26-Ich werde arbeitslos. Wie bin ich dann versichert_ _ Die Techniker.jpg (63.53 KiB) Viewed 7529 times

If you had chosen private health insurance once you exceeded the Versicherungspflichtgrenze income limit, i.e. if you had

not chosen to continue on as a voluntary member, through becoming unemployed and getting Arbeitslosengeld I, you would still become a mandatory member of public health&nursing insurance - but only as long as you are not already 55:

https://www.tk.de/techniker/leistungen- ... rn-2005734

There are also ways back into public health insurance for people over 55:

- if you have a spouse who is in public health insurance (no matter whether as a mandatory or as a voluntary member) and your monthly worldwide income is not more than 1/7 * Bezugsgröße, which in 2024 is 1/7 * 3,535€ = 505€ or you only have income from a 538€ mini job (that is the 2024 value, it will rise in the future, since they linked the mini job limit to the minimum wage, which rises every year), you can get back into public health insurance under free family insurance: https://www.tk.de/en/i-am-tk/family-mem ... ed-2052462

- if you move away from Germany, to an EU/EEA country that has public health insurance for everybody, e.g. to Austria or to the Netherlands, and you then stay in that EU/EEA public health insurance for more than 12 months, then you can move back to Germany and German public health insurance has to accept you as a member no matter how high your income is, since you are coming straight out of another EU/EEA's country's public health insurance system.

zeeshan wrote: ↑Fri Mar 29, 2024 4:40 pm

And in case I do need to pay the contributions, I pay it at the year end, right? So for year 2024, I'll pay it in 2025 once I have a tax certificate from the broker.

Yes.

Public health insurers usually ask voluntary members for a copy of their income tax Bescheid and they will then see that member's income from your capital assets in the Bescheid.

Re: Capital gains tax and health insurance

Posted: Sat Mar 30, 2024 1:43 pm

by zeeshan

Thanks PandaMunich for such a through explanation. I'm really glad I found the forum.

Some more questions, hope you won't mind: Will it also affect the unemployment and pension insurance contributions? And do you know how to pay for all these insurances now because it's always deducted automatically from my salary so I have no clue.

My health insurance also never asked for any income Bescheid ever so it never even occurred to me before. One more thing, I remember that if you use a German Broker then they automatically deduct capital gains on your behold and report it so you don't have to file/report it. Unlike income tax, I never filed any capital gains my self and also because it's under or may be 1-2 euro over the exemption limit. I don't see anything related to capital gains mentioned in my Bescheid from Finanzamt, I do have the tax certificate from my broker though. Any idea regarding it?

Re: Capital gains tax and health insurance

Posted: Sat Mar 30, 2024 2:28 pm

by PandaMunich

Pension insurance and unemployment insurance only charge based on your work income, in your case, based on your gross salary.

--> nothing to do there.

I suggest you just send your public health insurer the Steuerbescheinigung your broker sent you.

Re: Capital gains tax and health insurance

Posted: Sun Mar 31, 2024 7:07 pm

by zeeshan

Thank you so much!

Re: Capital gains tax and health insurance

Posted: Thu Apr 04, 2024 1:11 pm

by zeeshan

Just to update the thread in case someone also needs to know. I got off from a call with my insurance provider on how to submit the proof and they said I don't need to pay any contributions from my capital gains, being an employee you only have to pay from your salary. I asked again because all the sources mentioned here are very definite and clear that I need to, and she still said that no, only if you were receiving pensions then you needed to pay any contributions. Guess, I'm just lucky. I think others should still get in touch with their insurance just to be on a safe side.